Personal Finance

How to Balance Spending, Saving, and Investing Your Bonus?

Bonus season is creeping up…

01 Nov 2024

READ MORE0

Can A Spender and A Saver Live Happily Ever After Together?

29 Oct 2024

0

Are You Considering A Personal Loan? Here Are Some Important Questions To Ask Yourself First

24 Oct 2024

0

Considering Opening a Digital Bank Account? Here’s What You Need to Know

23 Oct 2024

0

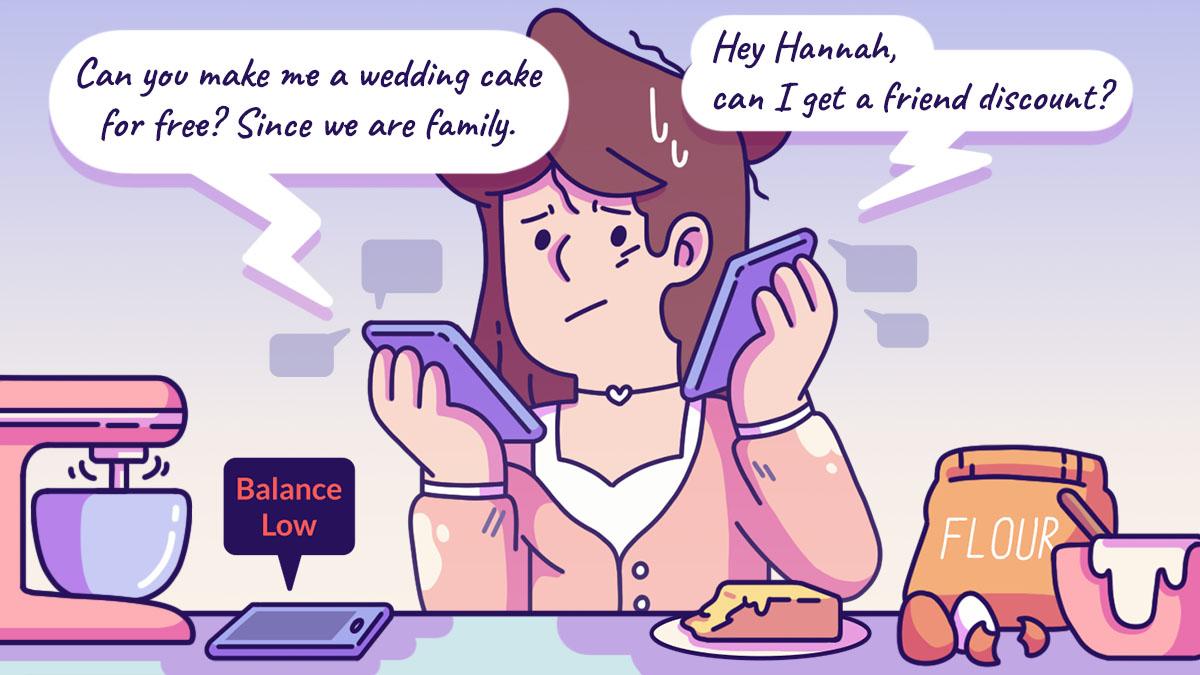

Being Too Nice Could Be Keeping You Poor

22 Oct 2024

0

Optimise Your Finances With A Multicurrency Account

21 Oct 2024

0

The Hidden Costs Of Remote Work

18 Oct 2024

0

Even Heroes Need Insurance Too

17 Oct 2024

0

What Are You Investing Your Resources On?

16 Oct 2024

0

Improve Your Financial Health With ‘Very Mindful, Very Demure’ Spending Habits

15 Oct 2024

0

SUBSCRIBE

STAY UPDATED!

And join our community© Copyright 2025 The Simple Sum. All Rights Reserved.